When a passenger clicks “I agree” during the airline booking process, do they unknowingly surrender their right to full compensation in the event of an accident? This question has gained significant legal traction in the aftermath of aviation disasters, where grieving families discover that buried within pages of digital terms and conditions lie clauses that attempt to limit their legal recourse. The enforceability of such digital agreements and their impact on victims’ rights presents a complex intersection of contract law, consumer protection legislation, and international aviation conventions.

The fundamental principle that must guide any legal analysis of these contracts is this: the act of accepting terms should never operate to extinguish the fundamental right to seek justice. The law ought not permit fine print to reduce human life to a mere contractual clause.

Understanding the Structure of Airline Ticket Contracts

When a passenger accepts terms and conditions during online flight booking, they enter into what courts have recognised as legally binding contracts. These ticket agreements form the civil foundation of the passenger-carrier relationship. Research indicates that approximately only 12% of consumers actually read these terms before acceptance, which transforms ticket agreements into what may fairly be described as a contractual black box containing complex legal obligations that most passengers neither understand nor consciously accept.

Airlines typically incorporate several categories of clauses that operate substantially in favour of the carrier. Limitation of liability provisions constitute a primary example, wherein airlines cap compensation for lost baggage at nominal amounts, often limited under international frameworks such as the Montreal Convention of 1999 to approximately 8.33 Special Drawing Rights per kilogram.

Mandatory arbitration clauses represent another significant category. Rather than permitting passengers access to local courts, airlines frequently mandate dispute resolution through arbitration in specified jurisdictions, commonly under Singaporean or American law. Such provisions materially restrict consumer access to convenient legal remedies and create an inherent imbalance favouring the airline.

Force majeure provisions operate to relieve airlines of liability for events deemed beyond their control, including natural disasters and pandemics. Exclusion of consequential damages typically prevents airlines from bearing responsibility for indirect losses such as missed events, interviews, or hotel reservations, unless clear fault can be established.

Class action waivers compound these restrictions by preventing passengers from combining their claims to challenge unfair practices collectively. Each aggrieved traveller must therefore pursue claims individually, even when the amounts involved make individual litigation economically impractical.

Judicial Scrutiny of Post-Accident Waivers

Following aviation accidents, passengers and their families frequently encounter contractual waivers that purport to limit their legal options. The enforceability of such waivers depends upon their ability to withstand judicial examination through established principles of contract law, including fairness, transparency, and the doctrine of unconscionability.

Courts have developed various legal tests for assessing waiver validity. A foundational principle under contract law holds that binding agreements must be entered voluntarily with free consent and must not be oppressive to either party. Consequently, unfair or concealed conditions, particularly those limiting liability or mandating arbitration in distant forums, may be declared unconscionable.

Case law has emphasised that unconscionable contract terms, especially those imposed upon weaker parties without genuine negotiation, are susceptible to being declared void. Judicial pronouncements have stressed that freedom to contract cannot be absolute; it must be balanced against the imperatives of justice and equity.

The Montreal Convention of 1999 establishes the foundational framework for airline liability in international carriage, providing passengers with minimum protections under Articles 17 to 21. These provisions create strict liability up to specified thresholds, currently approximately 128,821 Special Drawing Rights for bodily injury or death. Airlines cannot contractually limit passenger claims up to these thresholds, and any attempt to do so through waivers is generally voidable. Courts have consistently held that waivers contrary to statutory protections cannot be enforced, as mandatory international obligations take precedence over private contractual arrangements.

Legal practitioners challenging post-accident waivers should examine several fundamental considerations. Was the waiver conspicuously disclosed, or was it concealed within fine print? Did the passenger agree knowingly or under circumstances negating genuine consent? Was any negotiation possible, or did the contract operate on a take-it-or-leave-it basis? Does the bargain shock the conscience through its one-sided nature?

An effective litigation strategy should emphasise procedural unfairness and inequality of bargaining power while highlighting how the contested terms derogate from statutory or treaty protections. Courts demonstrate greater willingness to invalidate clauses that appear exploitative, particularly within the emotionally charged context of aviation disasters.

The Air India AI-171 Case: Digital Terms Under Judicial Examination

The tragic Air India Flight AI-171 crash illuminated not only aviation safety concerns but also the legal complexities surrounding digital ticket terms. The accident during descent into Ahmedabad resulted in multiple casualties and injuries. While investigation into causation continues, the families of victims have confronted substantial legal challenges regarding the enforceability of ticket terms and conditions.

The most contentious provision in the AI-171 ticket contract concerned mandatory arbitration in Bangalore with compensation capped at fifty thousand rupees. These conditions were embedded within digital booking platforms and were deemed “agreed to” when passengers or their representatives proceeded through the booking process. Following the crash, numerous grieving families expressed dismay upon discovering these limiting provisions.

Victim families approached the Bombay High Court, initiating legal proceedings that resulted in interim injunctions restraining Air India from enforcing the arbitration clause. The Court determined that enforcement of such a clause might amount to denial of substantive justice, particularly in the aftermath of a fatal incident. Public interest petitions filed in connection with the case characterised this arbitration requirement as a blanket denial of justice, given that families had no genuine opportunity to negotiate or review these terms.

The ticket contract bears the characteristics of an adhesion contract. Such contracts, particularly within consumer contexts, invite judicial scrutiny under doctrines of unconscionability and unfair surprise. Courts examine whether the weaker party genuinely had choice and whether terms were presented conspicuously.

The families contend that arbitration clauses and compensation caps were not merely buried from view but were fundamentally inadequate to address the anguish suffered. In practice, legal representatives may demonstrate procedural unfairness, absence of consent, and the undue burden placed upon victims. The magnitude of the tragedy itself weighs substantially against enforcement of rigid contractual provisions.

The AI-171 matter clarifies the necessity of scrutinising digital consent mechanisms in high-stakes contracts. It raises profound questions concerning justice, empathy, and the ethical boundaries within which aviation contracts may be enforced.

Contractual Issues in Major Aviation Disasters

Examination of significant airline disasters reveals that ticket terms and conditions have consistently been sources of legal dispute, particularly clauses relating to arbitration and liability limits. Such contractual provisions, frequently embedded within digital booking processes, have drawn judicial scrutiny across multiple jurisdictions.

In the Malaysia Airlines MH370 case, families were required to accept arbitration in Hong Kong as a condition for receiving partial compensation. This requirement attracted substantial criticism, with several families mounting legal challenges.

Following the Lion Air Flight JT610 crash in 2018 and the Ethiopian Airlines Flight 302 disaster in 2019, victims’ families initiated legal proceedings in the United States and other jurisdictions. Legal counsel successfully bypassed restrictive contractual provisions by invoking the Montreal Convention, particularly Articles 17 and 21 concerning airline liability. This approach enabled pursuit of claims within public judicial systems rather than private arbitration forums.

Across these tragedies, a discernible pattern emerges: digital acceptance mechanisms face increasing challenge from passengers and their legal representatives. In India, pleadings under the Consumer Protection Act of 2019 emphasise the absence of genuine consent and the unilateral nature of airline contracts. Families maintain that consumers are not meaningfully informed about dispute resolution clauses, let alone afforded opportunity to negotiate them. The legal trajectory demonstrates a gradual but perceptible shift toward protection of consumers from unfair contractual waivers.

The Distinction Between Carriage of Goods and Carriage of Passengers

A clear distinction must be drawn between contracts for carriage of goods and those for carriage of passengers. Under Indian contract law, a carrier dealing with goods may, by agreement, limit liability for loss or damage. Courts have respected such waivers in cargo cases, recognising that both parties entered arrangements with full understanding of associated risks. However, this principle has no application when passengers are concerned. Statutory protections intervene and override any contractual attempt to curtail rights.

The Carriage by Air Act of 1972, which incorporates the Montreal Convention, imposes strict liability upon airlines for death or bodily injury. Clauses seeking to cap compensation at token amounts or compelling grieving families into distant arbitration forums have repeatedly been tested against public policy, fairness, and the doctrine of unconscionability.

Recent jurisprudence reflects this principle. In Vinay Shankar Tiwari versus IndiGo Airlines (2013), the Uttar Pradesh State Consumer Disputes Redressal Commission held that airlines cannot rely upon digital acceptance mechanisms to contract away their duty of care or basic fairness. The Commission observed that while passengers are bound by terms of carriage, airline authorities should assist passengers in boarding scheduled aircraft after completion of security measures in a timely manner.

Consumer Protection Law and Digital Contracts

In the evolving legal landscape of airline disputes, Indian consumer law is increasingly employed to challenge restrictive terms in digital contracts. Traditional contract doctrines of privity and consent are being set aside in favour of alternative frameworks focusing upon fairness and consumer welfare under the Consumer Protection Act of 2019.

The Consumer Protection Act protects consumers against unfair trade practices, including digital contracts containing unilateral disclaimers and hidden clauses restricting legal remedies. The Act recognises the power imbalance inherent in standard form contracts and empowers consumer forums to invalidate terms that contravene public interest. Specifically, arbitration clauses or force majeure provisions that operate as instruments denying consumers access to justice may be declared void by these forums.

International Conventions and Global Consumer Protection

Cross-border air travel places passengers within the intersection of international treaties and domestic law. The Montreal Convention of 1999 leads this regulatory regime, standardising airline liability for injury, delay, and baggage loss. The Convention expressly prohibits carriers from contracting out of minimum liability thresholds, thereby establishing a baseline of protection for passengers.

Within the European Union, Regulation EC No. 261/2004 imposes additional obligations upon airlines, requiring compensation for cancellations, extended delays, and denied boarding. Airlines have attempted to circumvent these obligations through private agreements, but courts have consistently rejected such attempts. Following the 2015 Paris terror attacks, courts declared that rights under EU261 cannot be waived by contract. Consumer rights remained neither suspended nor waived even in circumstances involving acts of terror.

India faces jurisdictional complexity in this regard. While the Montreal Convention binds as a matter of international law, domestic enforcement is governed by the Carriage by Air Act of 1972, the Consumer Protection Act of 2019, and the Aircraft Rules of 1937. This complex interaction demonstrates how treaty-based rights and national consumer protections together strengthen passenger claims despite aggressive airline contracting practices.

Practical Guidance for Passengers and Legal Representatives

In the contemporary environment of online airline bookings, passengers and their legal representatives must remain vigilant regarding contractual terms. Most ticketing platforms embed extensive terms and conditions that include arbitration clauses, governing law provisions, and liability waivers, each carrying serious legal consequences.

Arbitration clauses and governing law provisions warrant particular attention, as they are typically buried within digital scroll boxes. Provisions designating foreign jurisdictions or arbitration seats can effectively deprive passengers of recourse under local law.

Such clauses may be challenged on principles of consumer protection and public policy, particularly under the Consumer Protection Act of 2019 and statutory Passenger Charter provisions.

Documentation is essential. Screenshots should be captured, timestamps recorded, and descriptions maintained of where disclaimers appeared on screen during booking. Such digital evidence may assist aggrieved parties in demonstrating that terms were not fairly disclosed.

Passengers should consider approaching local consumer forums rather than international arbitration centres. These forums provide cost-effective, rights-based remedies and have become increasingly assertive in refusing to enforce unfair airline contracts.

Policy Reform and the Path Forward

A progressive approach to airline contracting requires a combination of regulatory directives, judicial discipline, and industry self-regulation. The Directorate General of Civil Aviation could initiate directives requiring airline booking platforms to display arbitration clauses, liability waivers, and governing law terms prominently and upfront. Presenting these clauses to passengers before payment would counteract the practice of burying them within hyperlinked text.

Internationally, the International Civil Aviation Organisation could be encouraged to establish model directives on digital contract fairness, including disclosure standards and passenger consent mechanisms. Such initiatives would facilitate harmonisation of consumer protection mechanisms across jurisdictions.

Legislatively, India would benefit from introducing a Consumer Protection (Digital Contracts) Bill that explicitly addresses standard-form digital contracts to ensure fairness, transparency, and genuine consent in aviation services. Such legislation could further prohibit pre-dispute arbitration in consumer matters.

Courts will continue to play an essential role in invoking public policy to invalidate terms that are oppressive to passengers who possess no negotiating power whatsoever.

It must be acknowledged that aviation is not casual about safety. Organisations operating within the sector function under rigorous regulatory frameworks. Before any flight takes off, numerous inspections, certifications, and compliance checks occur, spanning airworthiness directives to routine and non-routine maintenance. These multiple layers exist precisely to ensure that catastrophic scenarios remain rare exceptions.

Several broader perspectives could further strengthen law and policy in this field.

Uniform Liability Standards: Extending Montreal-style compensation standards to domestic flights would prevent disparity between international and domestic passengers.

Advance Compensation Mechanisms: Mandating transparent advance payment mechanisms would provide families with immediate relief following accidents, avoiding unnecessary hardship and litigation delays.

Digital Contracting Fairness: Passenger contracts should highlight statutory rights prominently in plain language, making aviation a benchmark for consumer protection in digital commerce. Regulations should clarify what cannot be concealed within digital contracts, ensuring statutory protections remain inviolable.

Insurance Enforcement: Compliance with mandatory liability insurance must be strictly monitored to ensure remedies remain genuine and enforceable.

Awareness Initiatives: Periodic efforts by airlines and regulators to educate passengers about their rights, particularly in digital ticketing contexts, would substantially reinforce trust.

The fundamental debate is not about airlines evading responsibility, but about how law and regulation can continue to strike appropriate balance. Transparency at the time of contracting, combined with the robust technical safeguards already embedded within aviation practice, serves to protect both passengers and the industry. Clicking “I Agree” must never mean surrendering fundamental rights, and it should also remind us of the immense responsibility carriers shoulder in keeping every flight safe.

Conclusion

Airline ticket contracts frequently obscure unfair terms beneath digital interfaces, leaving passengers with limited recourse. The legal principles examined herein outline the mechanisms through which courts, regulators, and consumers may challenge such unfair terms.

The working definition of consent must require genuine understanding rather than merely click-induced, compelled acknowledgment. Strengthening of disclosure requirements, judicial vigilance, and statutory safeguards remains essential. Industry participants should promote transparency and fairness, while passengers must insist upon reading key terms, maintaining documentation, and enforcing their rights through consumer forums.

The time has arrived to rebalance the relationship between airlines and passengers. Contracts should serve people, not operate against them. Reform founded upon justice and transparency deserves collective support.

Frequently Asked Questions

Can airlines impose terms and conditions even if the passenger does not read them?

When a passenger clicks “I Agree,” contract law generally treats this as valid consent even if the terms were not read. However, courts retain authority to strike down clauses that are unfair or that violate statutory protections.

Can airlines completely avoid liability for crashes through contracts?

Airlines cannot completely exclude liability for crashes through contractual provisions. Domestic legislation such as the Carriage by Air Act of 1972 and international instruments such as the Montreal Convention establish minimum liability standards that cannot be waived contractually.

Do Indian passengers receive different protection compared to international passengers?

Yes, protection differs. International passengers receive protection under the Montreal Convention, which establishes uniform global liability standards. Indian passengers on domestic flights typically rely upon the Carriage by Air Act of 1972 and the Consumer Protection Act of 2019.

This article presents legal analysis for educational purposes. Specific legal matters should be addressed through consultation with qualified legal professionals.

Stay orders are temporary judicial interventions that pause enforcement of lower court judgments while appeals are pending, not permanent dismissals. Indian courts grant stays only when specific conditions are met: prima facie case, balance of convenience, and irreparable injury. As established in Asian Resurfacing (2018), stays automatically lapse after six months unless extended with recorded reasons. The Supreme Court emphasizes judicial restraint in granting stays, particularly in public interest matters. While stays preserve status quo and prevent irreparable harm during proceedings, they don’t determine case merits. Once vacated, the original judgment becomes immediately enforceable – a “sleeping lion that awakens.”

A stay order temporarily suspends the effect of a ruling, preserving the status quo while legal proceedings continue

The Indian judicial system, with its hierarchical structure of courts, provides various remedies to ensure justice and prevent irreparable harm during the pendency of legal proceedings. Among these remedies, the concept of ‘stay orders’ holds particular significance. Often misunderstood as a permanent solution, stay orders are essentially temporary judicial interventions that suspend the operation of a judgment, order, or legal proceeding while the matter is under review by a higher court.

Understanding the Nature of Stay Orders

A stay order is fundamentally different from a dismissal or quashing of a lower court’s decision. While the latter permanently invalidates a judicial pronouncement, a stay merely puts it on hold. This distinction was eloquently clarified by the Supreme Court in Asian Resurfacing of Road Agency Pvt. Ltd. v. Central Bureau of Investigation (2018) 16 SCC 299, where the Court observed that “a stay order does not render a decision of the lower court a nullity; it only suspends the enforceability of the order/judgment.”

The temporary nature of stay orders is rooted in the principle of maintaining status quo ante, preventing any party from suffering irreparable injury during the pendency of proceedings. The Supreme Court in Mulchand Deva Ram Chawla v. State of Gujarat (1974) 3 SCC 698 held that “the very purpose of a stay order is to preserve the subject matter of the appeal and to ensure that the appeal, if successful, is not rendered infructuous.”

Legal Framework Governing Stay Orders

The power to grant stay orders derives from multiple statutory provisions and inherent powers of courts. Under the Civil Procedure Code, 1908, Order XLI Rule 5 specifically empowers appellate courts to stay proceedings in execution of decrees. Section 151 of the CPC also provides inherent powers to courts to make such orders as may be necessary for the ends of justice.

In criminal matters, Section 397 read with Section 401 of the Code of Criminal Procedure, 1973, empowers High Courts and Sessions Courts to stay orders of subordinate courts during revision proceedings. Similarly, Article 226 and Article 227 of the Constitution vest High Courts with supervisory jurisdiction, including the power to grant interim stay orders.

The Supreme Court, under Article 136 of the Constitution, exercises its special leave jurisdiction and frequently grants stay orders pending final disposal of special leave petitions. In Gangadhar v. Raghunath (1981) 4 SCC 103, the Supreme Court emphasized that “the power to grant interim relief, including stay orders, is incidental to the main power of the Court to do complete justice between the parties.”

Conditions for Granting Stay Orders

Courts do not grant stay orders mechanically or as a matter of routine. The Supreme Court in Shiv Shakti Coop. Housing Society v. Swaraj Developers (2003) 6 SCC 659 laid down three essential conditions for granting stay:

A prima facie case in favor of the applicant

Balance of convenience tilting in favor of the applicant

Irreparable injury likely to be caused if stay is not granted

The Court further clarified that these conditions are cumulative and not alternative. The mere filing of an appeal or revision petition does not automatically entitle a party to a stay order. In Atma Ram v. State of Punjab (1959) SCR 1 SC, the Supreme Court held that “stays should be granted only in exceptional circumstances and not as a matter of course.”

Duration and Limitations of Stay Orders

Recognizing that prolonged stays can defeat the purpose of justice, courts have imposed temporal limitations on stay orders. The Supreme Court in Asian Resurfacing of Road Agency (supra) directed that any stay granted by any court, including the High Court, shall automatically lapse after six months unless extended for good reasons to be recorded in writing.

This landmark judgment aimed to prevent the misuse of stay orders, which often resulted in cases remaining pending for years. The Court observed that “stay orders cannot be allowed to operate indefinitely and defeat the very purpose of expeditious disposal of cases.”

In Commissioner of Central Excise v. Dunlop India Ltd. (1985) 1 SCC 260, the Supreme Court held that interim orders should not be continued mechanically without considering changed circumstances. The Court emphasized that “an interim order which was passed at an earlier stage may require modification or vacation in view of subsequent developments.”

Stay Orders versus Merits of the Case

It is crucial to understand that granting a stay order does not reflect upon the merits of the main case. The Delhi High Court in Rajiv Mehrotra v. Suresh Mehrotra 175 (2010) DLT 289 clarified that “grant of stay is not a reflection on the merits of the case, but is aimed at preserving the subject matter and preventing prejudice to parties during pendency of proceedings.”

The distinction between interim relief and final adjudication was highlighted by the Supreme Court in State of Maharashtra v. Digambar (1995) 4 SCC 683, where it held that “while granting interim relief, the Court does not decide the controversy on merits but merely preserves the property in dispute to await the final outcome of the proceedings.”

Vacation and Modification of Stay Orders

Stay orders, being temporary in nature, are subject to vacation or modification. The Supreme Court in M/s. Transcore v. Union of India (2006) 6 SCC 224 held that “a party can always approach the Court for vacation or modification of stay orders if there is change in circumstances or if the stay is being misused.”

Courts have inherent power to recall or modify their own orders, including stay orders. In Grindlays Bank Ltd. v. Income Tax Officer (1980) 2 SCC 191, the Supreme Court observed that “the power to grant stay necessarily implies the power to vacate or modify it when circumstances warrant such action.”

Impact on Lower Court Proceedings

When a stay order is issued, the proceedings or execution of orders of lower courts are temporarily suspended, but the original judgment remains intact. The Supreme Court in Kunhayammed v. State of Kerala (2000) 6 SCC 359 clarified that “a stay order does not wipe out the order of the lower court; it only suspends its operation.”

This principle ensures that if the appeal or revision is dismissed, the original order springs back to life without requiring any fresh proceedings. The Karnataka High Court in Smt. Leelavathi v. M. Chandrashekar ILR 2006 KAR 3426 aptly noted that “a stayed order is like a sleeping lion which wakes up the moment stay is vacated.”

Stay Orders in Different Jurisdictions

The principle that stay orders are temporary measures is consistent across various branches of law. In taxation matters, the Supreme Court in Commissioner of Income Tax v. Vallabh Glass Works Ltd. (1983) 2 SCC 410 held that “stay of recovery proceedings does not amount to stay of assessment; the assessment order remains valid and enforceable once the stay is lifted.”

In service law jurisprudence, the Supreme Court in State of Uttar Pradesh v. Brahm Datt Sharma (1987) 2 SCC 179 observed that “stay of operation of an order of punishment does not amount to setting aside the order; it merely postpones its implementation.”

Judicial Restraint in Granting Stays

Courts have increasingly emphasized the need for judicial restraint in granting stay orders. The Supreme Court in Siliguri Municipality v. Amalendu Das (1984) 2 SCC 436 cautioned that “courts should be extremely careful and circumspect in granting stay orders as they tend to upset the normal course of administration of justice.”

The principle of judicial restraint is particularly important in matters involving public interest. In State of Karnataka v. State of Tamil Nadu (2017) 3 SCC 362, the Supreme Court held that “while considering stay applications in matters of public importance, courts must balance private interests against larger public good.”

Abuse of Stay Orders and Judicial Response

The Indian judiciary has been cognizant of the potential misuse of stay orders. In T.N. Godavarman Thirumulpad v. Union of India (2006) 1 SCC 1, the Supreme Court expressed concern over the “stay order culture” and emphasized the need for stricter scrutiny before granting stays.

To prevent abuse, courts have started imposing conditions while granting stays. In Deccan Airways Ltd. v. Air Aviation Inter-City Services (1986) 3 SCC 423, the Supreme Court upheld the practice of imposing monetary conditions or requiring security deposits while granting stay orders.

Conclusion

The jurisprudential understanding of stay orders in India clearly establishes their temporary and provisional nature. They serve as a crucial tool for preserving the rule of law and preventing irreparable harm during the pendency of legal proceedings. However, they are not and cannot be construed as permanent relief or as a judgment on the merits of the case.

The evolution of judicial thinking on stay orders reflects a careful balance between providing necessary interim relief and ensuring that justice is not delayed indefinitely. The recent trend of imposing time limits on stay orders and requiring periodic review demonstrates the judiciary’s commitment to preventing their misuse while maintaining their effectiveness as a tool for interim relief.

As the Supreme Court eloquently stated in Mohd. Mehtab Khan v. Khushnuma Ibrahim Khan (2013) 9 SCC 221, “Stay is a temporary phase. It is an order to preserve the status quo till the matter is finally decided. It does not determine any right and is meant only to grant temporary relief.” This fundamental principle continues to guide the Indian judiciary in its approach to stay orders, ensuring that they remain true to their intended purpose as temporary judicial interventions rather than permanent solutions.

The clear jurisprudential position is that stay orders are bridges, not destinations – they facilitate the journey to justice but are not the final resting place of judicial determination. Understanding this distinction is crucial for both legal practitioners and litigants in navigating the Indian judicial system effectively.

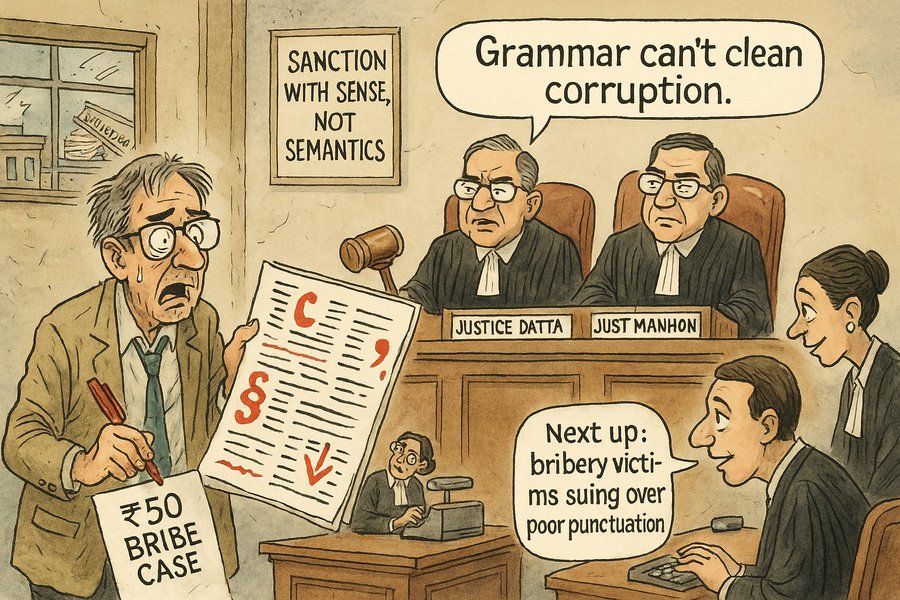

In a ruling that might disappoint grammar pedants everywhere, the Supreme Court has declared that minor edits don’t constitute a get-out-of-jail-free card for corrupt officials.

The Case of the Contested Commas

The Supreme Court recently dashed the hopes of a retired public servant who apparently believed that a red pen might accomplish what his defense counsel couldn’t. The official, convicted of accepting a modest ₹500 bribe back in 2000 (barely enough for a decent coffee these days), had pinned his acquittal hopes on alleged irregularities in the sanction order that authorized his prosecution.

Justices Dipankar Datta and Manmohan, clearly unimpressed by this editorial defense strategy, ruled that the minor tweaks made to the sanction report merely ensured its form matched its substance—a bit like adjusting your tie without changing your entire outfit.

Substance Over Style: The Court’s View

“If a draft order is placed before the sanctioning authority and he is satisfied that nothing needs to be added/deleted therefrom, the grant of sanction cannot be faulted merely on the ground of absence of addition of words to/deletion of words from the draft,” the Court declared, in what might be history’s most meta judicial statement about editing.

In essence, the Court concluded that the sanctioning authority had properly applied their mind before issuing the order—a refreshing assessment in bureaucratic circles, where “applying one’s mind” isn’t always a given.

The ₹500 Question

The case itself dates back to 2004 when a Special Court convicted the appellant for demanding and accepting a ₹500 bribe to expedite land record extracts. The Bombay High Court affirmed this conviction in September 2024, presumably after spending two decades contemplating the philosophical implications of a ₹500 bribe in an increasingly inflationary economy.

Before the Supreme Court, the appellant argued procedural flaws, including an allegedly “mechanical” sanction for prosecution—as if rubber stamps weren’t a time-honored tradition in government offices.

The Fine Print of Justice

Justice Datta, who authored the judgment, emphatically rejected claims that the sanction was granted without application of mind. The Court noted that sanctions exist to protect honest officials, not to provide a syntactical escape hatch for the dishonest ones.

“There is a legal impediment to prosecute a public servant for corruption, if there be no sanction,” the Court observed, before clarifying that all a sanctioning authority needs is to be satisfied about the existence of a prima facie case—not absolute certainty about every crossed ‘t’ and dotted ‘i’.

The Grammar of Corruption

Citing precedent from Manzoor Ali Khan v. Union of India, the bench emphasized that while procedural safeguards are important, they cannot become technical loopholes through which corruption slips unchecked.

“Even otherwise, merely because there is any omission, error or irregularity in the matter of granting sanction, that does not affect the validity of the proceedings unless the court records its own satisfaction that such error, omission or irregularity has resulted in a failure of justice,” the Court observed, essentially telling corruption defendants that their spell-check defense strategy needs a serious upgrade.

The Moral of the Story

In what might be considered a judicial version of “substance over form,” the Supreme Court has made it clear that minor alterations in a report, without any prejudice to substantial justice, don’t render a sanction order invalid.

For public servants contemplating similar appeals based on clerical technicalities, the message is crystal clear: editorial critiques won’t save you from corruption charges. Perhaps it’s better to simply avoid accepting bribes—even ones that wouldn’t cover a movie ticket in 2025’s economy.

The appellant, represented by Ms. Meenakshi Arora, senior counsel, might now be contemplating that ₹500 was an extremely expensive bribe—not for what it bought, but for what it ultimately cost.

Case Title: DASHRATH VERSUS THE STATE OF MAHARASHTRA

In a profession where words are the primary currency, the irony wasn’t lost on anyone when Chief Justice of India Sanjiv Khanna proclaimed that lawyers need to talk less—or at least write less. At a farewell function that could have easily devolved into ceremonial platitudes and nostalgic reminiscences, CJI Khanna instead delivered a masterclass on legal drafting that left many Advocates-on-Record (AoRs) frantically taking notes rather than clicking photographs.

“One thing I still feel we haven’t really mastered is the art of drafting,” declared CJI Khanna, his voice carrying the weight of countless nights spent wading through verbose petitions. “I feel a huge effort is required. We need to understand ‘less is more’…” The collective gulp from the audience was almost audible. In legal circles, where charging by the word has become something of an unspoken tradition, this was tantamount to suggesting barristers abandon their signature black robes.

European Efficiency vs. Indian Exuberance

To drive home his point, CJI Khanna shared an anecdote from his days as a practicing lawyer, when he drafted objections to an award in a European Court. With obvious pride, he mentioned drafting a mere “8 to 9 grounds” for objection—practically haiku-like brevity by Indian legal standards. Yet his European counterpart, likely stifling a chuckle, informed him that these would be further reduced to just three grounds. The reason? “The costs would be higher otherwise.”

This moment of cultural clash perfectly encapsulates the difference between European legal efficiency and Indian legal exuberance. While our European counterparts treat words as precious diamonds to be carefully selected and displayed, Indian legal documents often resemble a wholesale jewelry market where every conceivable ornament is on display, just in case something catches the judge’s fancy.

The Judicial Plea for Mercy

“We need to have crisper petitions. It helps us read the files more easily,” CJI Khanna continued, in what could only be interpreted as a judicial plea for mercy. One could almost visualize the Chief Justice’s chambers, buried under mountains of paperwork, each petition competing with the next in a Dickensian contest of verbosity.

The statement reveals a rarely acknowledged truth: judges are human beings with finite reading capacity and patience. Behind the grand robes and elevated benches are individuals who must process thousands of pages daily. CJI Khanna’s appeal wasn’t just professional advice; it was a humanitarian request.

The Curious Case of the Invisible AoRs

Having addressed the quantity of words, CJI Khanna turned his attention to who should be delivering them in court. In what might have caused several Senior Advocates to spill their coffee, he encouraged AoRs to argue matters themselves instead of merely serving as conduits to more experienced (and expensive) counsel.

“You have direct access to litigants. Why don’t you come and argue in the court yourself?” he asked pointedly. The question hung in the air like a challenge, addressing the elephant in the courtroom—the hierarchy that often relegates AoRs to background roles despite their intimate knowledge of cases.

This gentle provocation highlights a peculiar aspect of India’s legal ecosystem, where despite having invested considerable time and effort to earn the prestigious AoR qualification (which grants them exclusive right to file matters before the Supreme Court), many prefer to remain backstage, briefing Senior Advocates who then take center stage in courtrooms.

Specialization: The Antidote to Generalization

Never one to stop at criticism without offering solutions, CJI Khanna proceeded to prescribe a career development path for the assembled legal minds. “Domain specialization coupled with mastery of facts will take you ahead than oratory,” he advised, effectively dismantling the popular notion that successful lawyers are primarily silver-tongued orators.

“Every case does not need a huge constitutional principle. Most cases are decided on facts,” he added, a statement that might seem obvious but represents a paradigm shift in a legal culture often obsessed with grand constitutional interpretations over the nitty-gritty of factual details.

The CJI’s recommendation for mediation training further underscored his forward-thinking approach to legal practice. In a system notoriously burdened with backlogs, alternative dispute resolution mechanisms offer a promising avenue for both lawyers and litigants seeking quicker, less adversarial solutions.

The Succession of Mentorship

Perhaps the most poignant moment came when CJI Khanna spoke about mentorship. “Anyone with 15 years of experience must mentor juniors,” he said, introducing an almost mandatory element to what has traditionally been a voluntary relationship.

This statement reflects a growing concern about the sustainability of legal practice. As law firms grow larger and individual practice becomes more competitive, the art of mentorship—once the cornerstone of legal education—risks becoming a casualty of commercial pressures.

The Promise of Continued Guidance

In a touching moment that bridged his past and future, CJI Khanna offered his continued availability for legal consultation even after retirement. “If I have an office in the future, I will always be open to give legal advice. It will be my pleasure if you walk in and seek advice,” he said, revealing the mentor’s heart beating beneath the judge’s robe.

This offer stands in stark contrast to the common trajectory of retired judges, who often retreat into private arbitration practices or head government commissions. CJI Khanna’s willingness to remain accessible speaks volumes about his commitment to the development of legal practice beyond his tenure on the bench.

The Social Responsibility of Legal Privilege

CJI Khanna concluded his address with a reminder of lawyers’ social responsibility, urging them to provide free legal aid to those unable to afford it. “Lawyers have a license to practice law, but for that privilege and status, lawyers have an obligation to provide legal services to those without ability to pay…that should be the goal,” he emphasized.

In these words, CJI Khanna distilled the essence of legal practice—not merely as a profession or business, but as a service imbued with social responsibility. It was a fitting final note from a judge described by his successor, CJI-designate Justice Gavai, as embodying “transparency and inclusiveness.”

Legacy of Transparency

Justice Gavai’s tribute to CJI Khanna highlighted how he lived the principle that “the CJI is only the first amongst equals and not superior.” This praise was echoed by SCAORA President Vipin Nair, who drew parallels between CJI Khanna and his legendary uncle, Justice HR Khanna, known for his lone dissent during the Emergency—perhaps the most famous example of moral courage in Indian judicial history.

Nair specifically commended CJI Khanna for his transparency in handling the sensitive Justice Yashwant Varma issue, where “all documents” were put “in the public domain.” This reference to transparency in dealing with contentious matters within the judiciary itself demonstrates how CJI Khanna’s principles extended beyond mere courtroom management to institutional governance.

The Final Gavel

As CJI Khanna prepares to demit office on May 13, 2025, his farewell address serves not just as a goodbye but as a roadmap for the future of legal practice in India. From crisp drafting to specialized practice, from mentorship to social responsibility, he has outlined a vision that balances tradition with innovation, expertise with accessibility.

In a profession often accused of being resistant to change, CJI Khanna’s parting words serve as both challenge and inspiration. As the legal fraternity bids farewell to his leadership, the true measure of his impact will be seen in how many take his advice to heart—writing shorter petitions, arguing their own cases, specializing their practice, mentoring juniors, and extending legal services to those who need them most.

After all, in CJI Khanna’s own words, “less is more”—except, perhaps, when it comes to the scope of one’s professional ethics and social responsibility. There, more is indeed more.

India’s labour law framework has undergone a historic transformation with the codification of 29 central labour laws into four comprehensive codes: the Code on Wages, 2019, the Industrial Relations Code, 2020, the Code on Social Security, 2020, and the Occupational Safety, Health and Working Conditions (OSHWC) Code, 2020. These reforms aim to streamline a historically complex and fragmented regulatory system, enhance the Ease of Doing Business (EoDB), foster industrial flexibility, and extend protections to India’s vast unorganized workforce, which comprises over 90% of the labour force—approximately 500 million workers. This article provides an in-depth analysis of the reforms’ objectives, provisions, potential benefits, challenges, and international lessons, concluding with actionable recommendations to ensure their successful implementation.

The Imperative for Reform: Unraveling a Legacy System

A Labyrinth of Laws

Prior to the codification, India’s labour regulatory landscape was a patchwork of over 40 central and 100 state laws, many dating back to the colonial era, such as the Factories Act (1881, revised 1948) and the Mines Act (1901, revised 1952). This multiplicity created overlapping jurisdictions, inconsistent definitions (e.g., “wages,” “employee,” “establishment”), and significant compliance burdens, particularly for Micro, Small, and Medium Enterprises (MSMEs). For instance, the Industrial Disputes Act (IDA), 1947, required government approval for layoffs, retrenchment, or closures in firms with 100 or more workers, a provision widely criticized by industry for stifling flexibility. This rigidity was believed to encourage firms to remain small (a phenomenon termed “dwarfism”), rely heavily on contract labour, or adopt capital-intensive technologies to avoid regulatory thresholds.

The complexity was compounded by definitional inconsistencies across statutes, leading to legal ambiguity and disputes. Businesses operating across states faced a patchwork of compliance requirements, disproportionately affecting MSMEs, which often lacked the resources for legal expertise. Larger corporations, with dedicated legal teams, navigated the system more easily, highlighting an uneven playing field that hindered economic scalability and formalization.

Exclusion of the Informal Workforce

A defining flaw of the pre-reform system was its limited reach, covering primarily the organized sector (less than 10% of the workforce). The Periodic Labour Force Survey (PLFS) 2022-23 estimated over 465 million informal workers, many earning below ₹5,000/month, with 27.5% earning less than ₹3,000/month according to PLFS 2023-24. These workers—spanning agriculture, small enterprises, home-based work, and casual labour—were largely excluded from statutory protections like minimum wages, social security (e.g., provident fund, insurance), or workplace safety standards. This exclusion perpetuated a dualistic labour market: a small, protected formal sector and a vast, precarious informal sector.

The vulnerability of informal workers was starkly exposed during the COVID-19 pandemic, particularly among inter-state migrant workers (ISMWs). The lack of portable benefits and social safety nets led to significant distress, with reports documenting 972 deaths during reverse migration. This crisis underscored the urgent need for a more inclusive labour framework that addresses the needs of India’s informal majority.

Economic and Governance Drivers

The reforms were propelled by India’s ambition to climb the World Bank’s EoDB rankings, attract foreign and domestic investment, and align with national initiatives like “Make in India,” “Digital India,” and “Startup India.” The government’s “Minimum Government, Maximum Governance” philosophy emphasized reducing bureaucratic hurdles, streamlining regulations, and leveraging technology, such as the e-Shram portal for worker registration. Simultaneously, the reforms aimed to achieve social justice by extending protections to informal, gig, and platform workers, aligning with the Second National Commission on Labour (SNCL) recommendations for consolidating laws into thematic codes.

The dual objectives—enhancing business ease and expanding worker welfare—reflect a philosophical shift from a fragmented, protectionist model to one aiming for universal applicability, simplification, and a balance between market-driven flexibility and baseline protections. This ambitious undertaking seeks to modernize India’s labour governance to support its goal of becoming a $5 trillion economy while addressing deep-rooted inequities.

The Four Labour Codes: A Detailed Examination

1. Code on Wages, 2019: Universalizing Wage Protections

Objective and Scope: Enacted in August 2019, the Code on Wages consolidates four laws: the Payment of Wages Act, 1936, Minimum Wages Act, 1948, Payment of Bonus Act, 1965, and Equal Remuneration Act, 1976. It aims to universalize minimum wage entitlements, ensure timely payments, standardize wage definitions, and promote gender equity across all sectors.

Key Provisions:

Unified Wage Definition: Defines “wages” as basic pay, dearness allowance, and retaining allowance, capping exclusions (e.g., bonuses, PF contributions, overtime) at 50% of total remuneration to prevent artificial wage suppression for statutory dues like provident fund and gratuity.

National Floor Wage: Empowers the central government to set a baseline wage, considering living standards (e.g., food, housing, clothing for a family of three). States must set minimum wages above this floor, reducing regional disparities.

Gender Equity: Prohibits wage discrimination based on gender for similar work, aligning with ILO Convention No. 100.

Compliance Simplification: Reduces paperwork, mandates electronic wage payments, and caps permissible deductions at 50% of wages.

Overtime and Bonus: Ensures overtime wages at twice the normal rate and a minimum bonus of 8.33% of annual wages for eligible employees.

Socio-Economic Context: PLFS data highlights severe wage challenges: 53.5% of workers earn below the MNREGS benchmark (~₹9,000/month), and women face a 20–33% gender wage gap. Rural-urban disparities are significant, with urban wages often double rural ones. The national floor wage aims to address these issues, but its impact depends on setting an adequately high level and robust enforcement, particularly in the informal sector where compliance is historically weak.

Potential Impact: The code could uplift millions of low-wage workers, reduce gender and regional disparities, and simplify employer compliance. However, challenges include potential state resistance to high floor wages due to investment competitiveness, ambiguity in calculating the 50% exclusion cap, and enforcement gaps in unregistered enterprises.

2. Industrial Relations Code, 2020: Balancing Flexibility and Harmony

Objective and Scope: Enacted in September 2020, this code consolidates the Trade Unions Act, 1926, Industrial Employment (Standing Orders) Act, 1946, and IDA, 1947. It seeks to streamline dispute resolution, enhance labour market flexibility, formalize trade union recognition, and promote industrial peace.

Key Provisions:

Retrenchment Threshold: Raises the limit for government approval for layoffs, retrenchment, or closures from 100 to 300 workers, easing flexibility for mid-sized firms.

Fixed-Term Employment (FTE): Legalizes FTE across industries, granting pro-rata benefits (e.g., PF, ESI) but excluding contract expiry from retrenchment protections, potentially increasing precariousness.

Trade Union Recognition: Designates a union with 51% worker support as the Sole Negotiating Union or forms a Negotiating Council for unions with 20%+ support, aiming to streamline bargaining.

Worker Re-skilling Fund: Employers contribute 15 days’ wages per retrenched worker to fund retraining.

Strike Regulations: Extends the mandatory notice period for strikes to 14 days for all establishments and classifies mass casual leave by 50%+ workers as a strike.

Case Study: Rajasthan’s Reforms: Rajasthan’s 2014 increase in the retrenchment threshold to 300 workers offers insights. An NIPFP study noted a 12% employment increase in large firms, but other analyses, like Goswami and Paul (2020), found increased contract labour and reduced overall labour use in export-oriented firms. Goldar (2024) argued that relaxed regulations boosted manufacturing jobs, illustrating mixed outcomes.

Stakeholder Perspectives: Industry welcomes the flexibility, citing reduced exit barriers. However, trade unions criticize the weakened job security for workers in firms with 100–300 employees and the potential for FTE to create “permanently temporary” roles. The decline in union density (from 19% in 1993 to 12.5% in 2014, per ILO estimates) raises concerns about diminished collective bargaining power.

Potential Impact: The code could stimulate formal sector hiring by reducing regulatory barriers, but risks exacerbating labour market dualism, with stronger protections for large-firm workers and increased precarity for others. The Worker Re-skilling Fund is promising but requires robust administration to align training with market needs, given past challenges with initiatives like Skill India.

3. Code on Social Security, 2020: Extending the Safety Net

Objective and Scope: Enacted in September 2020, this code consolidates nine laws, including the Employees’ Provident Funds Act, 1952, Employees’ State Insurance Act, 1948, and Unorganised Workers’ Social Security Act, 2008. It aims to universalize social security, notably including gig and platform workers for the first time.

Key Provisions:

Gig/Platform Worker Inclusion: Defines gig workers (freelancers outside traditional employment) and platform workers (engaged via online platforms like Uber, Zomato). NITI Aayog estimates 7.7 million such workers in 2020-21, projected to reach 23.5 million by 2029-30.

e-Shram Portal: A national database with over 300 million registered unorganized workers, providing a Universal Account Number (UAN) for accessing benefits like health, maternity, and pensions.

Social Security Funds: Central fund for gig/platform workers and state funds for unorganized workers, partially funded by a 1–2% aggregator levy (capped at 5% of payouts).

Mandatory Registration: Workers register via e-Shram, with Aadhaar mandatory for benefit access.

Socio-Economic Context: The gig economy’s rapid growth underscores the code’s relevance. These workers face income instability, no minimum wage guarantees, and exclusion from traditional benefits. Women, constituting 53.68% of e-Shram registrations, are particularly vulnerable to low earnings (e.g., rural self-employed women earn ~₹5,000/month).

Case Study: Karnataka’s Gig Worker Bill: Karnataka’s 2024 draft bill mandates a 1–2% welfare levy on aggregators, offering a state-level model. However, debates over turnover definitions and compliance complexity highlight challenges scalable to the national level.

Potential Impact: The code’s inclusion of gig workers is groundbreaking, but funding adequacy is a concern. The FY 2023-24 allocation of ₹350 crore is dwarfed by the target population’s scale. The Union Budget 2025-26’s expansion of PMJAY health coverage to 10 million gig workers is a step forward, but sustainable financing remains unresolved. Administrative integration across states and portability of benefits are critical for success.

4. Occupational Safety, Health and Working Conditions (OSHWC) Code, 2020

Objective and Scope: Enacted in September 2020, this code consolidates 13 laws, including the Factories Act, 1948, Mines Act, 1952, and Inter-State Migrant Workmen Act, 1979. It aims to enhance workplace safety, health, and conditions across establishments with 10+ workers.

Key Provisions:

Employer Duties: Mandates hazard-free workplaces, free annual health check-ups for hazardous sectors, and welfare facilities (e.g., canteens, crèches).

Appointment Letters: Requires formal letters for all employees, promoting formalization.

Inspector-cum-Facilitator: Shifts to a facilitative enforcement model with web-based, risk-based inspections.

Ground Reality: A CAG 2022 report found only 35% of factories fully compliant with safety norms. High-risk sectors like construction and sanitation, employing over 60% of workers, face elevated morbidity. Sanitation workers, often from marginalized castes, face extreme hazards, with an estimated 2 million in high-risk roles.

Case Study: Migrant Worker Crisis: The COVID-19 lockdowns exposed ISMW vulnerabilities, with millions stranded without support. The code’s portability provisions are a response, but effective inter-state coordination remains a hurdle.

Potential Impact: The code strengthens safety standards and formalization, but its 10-worker threshold excludes micro-enterprises, a significant informal sector segment. Enforcement capacity and digital infrastructure are critical for realizing benefits.

Potential Benefits of the Reforms

Simplified Compliance: Consolidating 29 laws into four reduces administrative burdens, potentially lowering compliance costs by 20–30% for MSMEs, per industry estimates.

Economic Growth: Enhanced flexibility and EoDB could attract FDI, supporting “Make in India” and manufacturing growth.

Social Inclusion: Universal minimum wages and social security for informal workers could reduce poverty and inequality.

Formalization and Digitization: Mandatory appointment letters and e-Shram registration promote formal employment, with over 30 crore workers already registered.

Implementation Challenges

1. Centre-State Harmonization

Labour’s Concurrent List status requires states to align rules with central codes. As of early 2025, 24–31 states/UTs have drafted rules, targeting finalization by March 31, 2025. Variations could recreate fragmentation, undermining the codes’ uniformity goal. Political differences across states add complexity.

2. Enforcement Capacity

The Inspector-cum-Facilitator model requires retraining thousands of officials and robust digital platforms. Historical enforcement weaknesses, especially in the informal sector, risk undermining compliance. The V.V. Giri National Labour Institute’s training programs are a start, but scaling is essential.

3. Funding Gaps

The Code on Social Security’s universalization ambition lacks clear financing. The 1–2% aggregator levy is debated for sufficiency, and FY 2023-24’s ₹350 crore allocation is inadequate for millions of workers. International models (e.g., US Social Security’s 12.4% payroll contribution) suggest higher, tripartite contributions.

4. Worker Rights Concerns

Increased retrenchment flexibility and FTE may weaken job security, particularly for workers in firms with 100–300 employees. Stricter strike rules and union recognition thresholds could reduce collective bargaining power, with union density already low at 7‒12.5%.

5. Digital and Administrative Integration

The e-Shram portal’s success depends on data accuracy, accessibility, and interoperability with state systems. Ensuring benefit portability (e.g., PDS, ESI, EPF) across states requires overcoming technological and governance barriers.

International Lessons: Pathways and Pitfalls

Indonesia’s Omnibus Law (2020)

Indonesia’s law aimed to simplify regulations and attract FDI but faced backlash for prioritizing flexibility (e.g., easier terminations, reduced severance) over worker rights. The Constitutional Court’s 2021 ruling declared it “conditionally unconstitutional” due to inadequate public consultation, forcing revisions. Lesson: Robust social dialogue is critical to avoid resistance and ensure legitimacy.

Brazil’s Labour Reform (2017)

Brazil’s reform liberalized outsourcing and introduced flexible contracts, aiming to boost jobs. However, it increased precariousness, reduced real wages, and weakened unions, with no significant formal employment growth. Lesson: Flexibility without strong social protections can exacerbate inequality and dual labour markets.

Vietnam’s Social Protection Expansion (2012–2020)

Vietnam achieved high health insurance coverage through mandatory contributions, state subsidies, and scheme integration. Challenges persisted in reaching informal workers, but political commitment drove success. Lesson: Sustainable financing and phased implementation are key to universal coverage.

Recommendations for Effective Implementation

National Labour Code Implementation Council Establish a council with Central, State, employer, and worker representatives to harmonize rules, resolve disputes, and monitor implementation. It should operate as a permanent body, adapting rules based on feedback and emerging labour market trends. Example: The council could mediate state variations in minimum wage fixation to ensure national coherence.

Labour Law Facilitation Cells for MSMEs Create cells via SIDBI and NSIC to provide MSMEs with compliance support, including workshops, helplines, templates, and compliance software. These cells should integrate business development advice, helping MSMEs leverage flexibility provisions (e.g., FTE) strategically. Example: SIDBI’s existing MSME financing network could host regional compliance clinics.

₹5,000 Crore Social Security Transition Fund Seed a fund to kickstart social security schemes, matching state contributions and co-funding aggregator levies. Governance should ensure transparency and alignment with long-term financing (e.g., payroll-based contributions). Example: The fund could finance e-Shram enrollment drives and initial health insurance for gig workers.

Capacity Building and Digital Infrastructure Invest in training Inspector-cum-Facilitators for advisory roles and scaling digital platforms like e-Shram. Develop mobile apps for worker redressal and interoperable databases for benefit portability. Example: Partner with tech firms to enhance e-Shram’s user interface and data security.

Staggered Rollout Strategy Implement codes in phases, starting with Wages and Social Security, and by firm size (large → medium → small) over three years. Clear timelines and support mechanisms (e.g., MSME cells) are crucial to minimize disruption. Example: Pilot implementation in urban industrial clusters before rural rollout.

Stakeholder Engagement and Awareness Launch nationwide campaigns to educate employers, workers, and unions about their rights and obligations. Engage trade unions in rule-making to build trust and reduce resistance. Example: Use media and community organizations to promote e-Shram registration among rural workers.

Conclusion: From Vision to Reality

India’s Labour Code reforms are a landmark effort to modernize a fragmented system, aligning labour governance with economic aspirations and social equity goals. By simplifying compliance, enhancing flexibility, and extending protections to informal and gig workers, the codes promise to transform India’s labour market. However, their success depends on overcoming significant challenges: harmonizing Centre-State rules, strengthening enforcement, securing sustainable funding, and balancing flexibility with worker rights.

International experiences—Indonesia’s cautionary tale, Brazil’s mixed outcomes, and Vietnam’s success—offer valuable lessons. The recommended strategies—a National Implementation Council, MSME facilitation, a transition fund, capacity building, staggered rollout, and stakeholder engagement—provide a roadmap for effective realization. With sustained political will, administrative diligence, and inclusive dialogue, India can translate these legislative promises into a dynamic, equitable labour market that supports its vision of inclusive growth and global economic leadership.

References

India’s New Labor Codes Enactment Status and Delayed Implementation, accessed May 4, 2025.

REFORM AND CODIFICATION OF India’s Labour Laws, cloudfront.net, accessed May 4, 2025.

Overview of Labour Law Reforms, PRS India, accessed May 4, 2025.

Changing Paradigm of the Labour Laws in India: A legal Analysis, ResearchGate, accessed May 4, 2025.

The Code on Wages, 2019, PRS India, accessed May 4, 2025.

The Industrial Relations Code, 2020, PRS India, accessed May 4, 2025.

The Code on Social Security, 2020, PRS India, accessed May 4, 2025.

The Occupational Safety, Health and Working Conditions Code, 2020, PRS India, accessed May 4, 2025.

Impact of Labour Reforms on Industry in Rajasthan, PHD Chamber, accessed May 4, 2025.

India’s Booming Gig and Platform Economy, NITI Aayog, accessed May 4, 2025.

E-Shram: One Stop Solution for Unorganised Workers, PIB, accessed May 4, 2025.

Indian States, UTs to Finalize Labor Codes Rules by March 2025, India Briefing, accessed May 4, 2025.

Indonesia’s Omnibus Law on Job Creation, Hogan Lovells, accessed May 4, 2025.

Brazil’s Labor Reform: How It’s Impacting the Job Market, Global People Strategist, accessed May 4, 2025.

Integrating Social Health Protection Systems Lessons Learned, accessed May 4, 2025.

3 in 4 Indian Labourers Earn Less Than Rs 15,000 A Month, Outlook Business, accessed May 4, 2025.

Article 254 of the Constitution of India stands as the cornerstone provision for addressing and resolving inconsistencies that arise between laws enacted by the Parliament of India (Union legislature) and those enacted by the Legislatures of the States.1 Its existence is fundamental within India’s constitutional architecture, often characterized as ‘quasi-federal’.3 This characterization stems from a structure that, while dividing powers between the Union and the States, also establishes significant areas of shared legislative authority and retains certain centralizing features.5 Article 254 provides the specific mechanism to manage conflicts within this framework, particularly in the domain where both levels of government are competent to legislate.6 The provision finds its roots in Section 107 of the Government of India Act, 1935, indicating a continuity in addressing legislative overlap from the pre-Independence era.6

The very presence and detailed nature of Article 254 underscore the foresight of the Constitution’s framers. They anticipated the potential for considerable legislative friction, especially concerning subjects placed in the Concurrent List of the Seventh Schedule.8 The Constitution meticulously delineates legislative powers through Article 246 and the three lists in the Seventh Schedule – the Union List, the State List, and the Concurrent List.11 The deliberate inclusion of a substantial Concurrent List, granting simultaneous legislative power to both the Union and the States over numerous important subjects 10, inherently created a zone of potential conflict. Article 254 was thus not an incidental provision but a carefully designed instrument to regulate this anticipated overlap.1 It establishes a clear, albeit complex, hierarchy and procedure for resolving conflicts, aiming to balance the need for national uniformity with the space for state-level legislative action within the quasi-federal structure.3 The nuanced exception provided in clause (2) further suggests a sophisticated approach beyond simple central dominance.

2/3 Significance in Concurrent Legislation

The primary operational sphere of Article 254 is the Concurrent List (List III of the Seventh Schedule).1 This list enumerates subjects upon which both Parliament and State Legislatures are competent to make laws.8 The rationale for a concurrent list includes the need for uniformity in basic laws across the country while allowing for state-specific variations where necessary. However, this shared legislative space inevitably leads to situations where a law made by a State Legislature may conflict with a law made by Parliament on the same subject. Article 254 provides the constitutional rule to determine which law prevails in such instances.7

It is crucial to distinguish conflicts under Article 254 from issues of legislative competence. If Parliament legislates on a matter exclusively reserved for the States (List II), or a State legislates on a matter exclusively reserved for the Union (List I), the resulting law is typically challenged as being ultra vires (beyond powers) the concerned legislature under Article 246.6 Repugnancy under Article 254, conversely, arises when both Parliament and the State Legislature are constitutionally competent to enact laws on the subject (i.e., a matter in the Concurrent List), but the provisions of their respective laws are inconsistent.6

3/3 Report Scope and Structure

This report provides an expert-level analysis of Article 254 of the Constitution of India. It commences with the full text of the Article, followed by a detailed examination of the doctrine of repugnancy, including its definition and the conditions under which it arises. The report then delves into the mechanism of Presidential assent provided under Article 254(2) and the overriding power retained by Parliament under the proviso. A significant portion is dedicated to analyzing the interpretation of Article 254 by the Supreme Court of India through landmark judgments. Furthermore, the report explores the crucial interlinkages between Article 254, Article 246, and the Seventh Schedule, assessing the impact of Article 254 on the federal balance of legislative power. Finally, it evaluates the role and significance of Article 254 within the broader context of Indian federalism and the principle of Parliamentary supremacy.

II. The Constitutional Provision: Text of Article 254

A. Presentation of Full Text

Article 254 of the Constitution of India reads as follows 15:

254. Inconsistency between laws made by Parliament and laws made by the Legislatures of States

(1) If any provision of a law made by the Legislature of a State is repugnant to any provision of a law made by Parliament which Parliament is competent to enact, or to any provision of an existing law with respect to one of the matters enumerated in the Concurrent List, then, subject to the provisions of clause…source any provision repugnant to the provisions of an earlier law made by Parliament or an existing law with respect to that matter, then, the law so made by the Legislature of such State shall, if it…source

B. Structural Breakdown

The structure of Article 254 is logical and hierarchical:

Clause (1): Establishes the general principle of Union supremacy in the event of a conflict between a State law and a competent Parliamentary law (or an existing law) concerning a matter in the Concurrent List. It declares the State law void to the extent of the repugnancy.

Clause (2): Carves out a specific exception to the general rule laid down in Clause (1). It allows a State law, despite being repugnant to an earlier Parliamentary law or existing law on a Concurrent List matter, to prevail within that State, contingent upon receiving Presidential assent after being reserved for consideration.

Proviso to Clause (2): Qualifies the exception in Clause (2). It reaffirms Parliament’s plenary power to legislate on the same Concurrent List matter subsequently, even to the extent of amending or repealing the State law that had received Presidential assent.

III. The Doctrine of Repugnancy: Defining Legislative Conflict

A. Meaning and Definition

The core concept underpinning Article 254 is ‘repugnancy’. In constitutional law, repugnancy signifies an inconsistency, incompatibility, contradiction, or direct opposition between the provisions of two different laws.6 It arises when laws enacted by two different legislative bodies, operating within a sphere of concurrent jurisdiction, cannot stand together.2 Black’s Law Dictionary defines “repugnant” as “inconsistent or irreconcilable with,” while Wharton’s Law Lexicon describes it as occurring when provisions in different laws conflict directly.6

Essentially, a situation of repugnancy emerges when applying two laws to the same set of facts yields contradictory outcomes, or when compliance with one law necessitates the violation of the other.2 It is this irreconcilable conflict in the concurrent field that Article 254 seeks to resolve.2

B. Conditions for Repugnancy

The Supreme Court of India, through numerous judgments, has delineated the conditions under which repugnancy can be said to exist between a Union law and a State law, primarily in the context of the Concurrent List.6 The mere possibility of conflict is insufficient; a demonstrable inconsistency is required. The key tests are:

Direct Conflict/Collision: There must be a clear and direct contradiction between the provisions of the Central Act and the State Act.2 The inconsistency must be “irreconcilable,” meaning the two laws are mutually exclusive and cannot be obeyed simultaneously.6 If it is possible to obey both laws without transgressing either, repugnancy generally does not arise.2

Occupying the Same Field: Both the Parliamentary law and the State law must operate in the same legislative field or pertain to the same subject matter.6 If the two laws deal with distinct aspects or operate in different domains, even if related, there might be no repugnancy. However, the laws need not fall under the identical entry in the Concurrent List if their substance covers the same ground.6

Intention to Cover the Field (Exhaustive Code): Repugnancy may also arise if Parliament, in enacting its law, intended to cover the entire subject matter comprehensively, leaving no room for State legislation in that field.6 If a Central law is deemed to be an exhaustive code on a particular subject in the Concurrent List, any State law on that subject, even if not directly contradictory in every detail, may be considered repugnant and thus void.2 This test focuses on the legislative intent behind the Parliamentary enactment.

These conditions were notably summarized by the Supreme Court in cases like M. Karunanidhi v. Union of India (1979) and derived from earlier pronouncements like Deep Chand v. State of U.P. (1959), which adapted principles from comparative constitutional law.2

The relatively high threshold established by the courts for finding repugnancy—requiring an “irreconcilable” conflict or “direct collision”—suggests a judicial preference for harmonious construction. Courts often endeavor to interpret Central and State laws in a manner that allows both to operate concurrently, thereby avoiding the invalidation of State legislation where possible.1 This interpretive approach can be seen as bolstering the federal principle by preserving State legislative space unless a conflict is unavoidable and absolute. The judgment in M. Karunanidhi, for instance, found that the State Act under challenge supplemented rather than contradicted the Central Acts, allowing both to stand.5

However, the principle that Parliament can ‘occupy the field’ introduces a significant dimension based on legislative intent.2 This allows Parliament to assert dominance over a Concurrent List subject by enacting legislation that is so comprehensive in scope that it implicitly signals an intention to exclude any State law in that area, even without direct contradiction in every clause.6 This serves as a potent tool for ensuring national uniformity when deemed necessary by Parliament. Landmark cases like Zaverbhai Amaidas v. State of Bombay (1954) and Forum for People’s Collective Efforts v. State of W.B. (2021) exemplify this, where State laws were invalidated because Parliament was deemed to have intended its legislation to be exhaustive in the respective fields.2

C. Scope of Invalidity

An important aspect of Article 254(1) is that it renders the State law void only “to the extent of the repugnancy”.1 This means that if only certain provisions of a State Act conflict with a Central Act, only those provisions become void, and the rest of the State Act may remain valid and enforceable, provided it can stand independently.2 The entire State statute is not automatically invalidated unless the repugnant provisions are inextricably linked to the rest of the Act.1

IV. The Presidential Assent Mechanism: Article 254(2)

A. The Exception to Parliamentary Supremacy

Article 254(2) provides a crucial, albeit conditional, exception to the general rule of Parliamentary supremacy established in Article 254(1).1 It allows a law made by a State Legislature concerning a matter in the Concurrent List to prevail within that specific State, even if its provisions are repugnant to those of an earlier law made by Parliament or an existing law (laws in force before the Constitution’s commencement) on the same matter.5 This mechanism acknowledges the possibility that a State may have legitimate reasons to enact legislation differing from pre-existing national norms on concurrent subjects.2

B. Conditions for Application

For a State law to benefit from the protection offered by Article 254(2), several conditions must be met cumulatively:

Concurrent List Matter: The State law must pertain to one of the matters enumerated in List III (Concurrent List) of the Seventh Schedule.1

Repugnancy with Earlier Central/Existing Law: The State law must contain provisions that are repugnant to the provisions of an earlier law made by Parliament or an existing law concerning that matter.1

Reservation for President’s Consideration: The Bill, after being passed by the State Legislature, must have been reserved by the Governor of the State for the consideration of the President of India.1

Receipt of President’s Assent: The President must have given his assent to the reserved Bill.6

If all these conditions are satisfied, the State law, despite its repugnancy to the earlier Central or existing law, will prevail and be operative within the boundaries of that particular State.1

C. The Role and Scope of Presidential Assent

The requirement of Presidential assent under Article 254(2) is not merely procedural; it involves substantive consideration. The President grants assent based on the aid and advice tendered by the Union Council of Ministers, as mandated by Article 74 of the Constitution.3 This effectively means that the Union executive plays a decisive role in determining whether a State should be permitted to deviate from an existing national legislative framework on a concurrent subject.